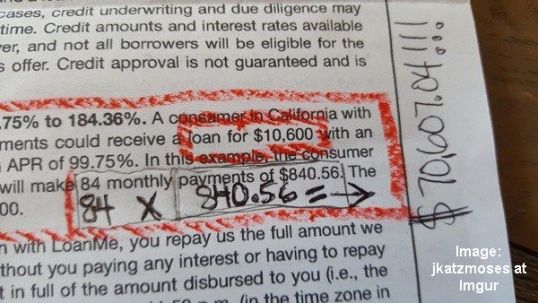

I recently had brought to my attention the existence of a company called “LoanMe,” which pre-qualified a redditor for a $10,600 loan at an APR of 99.75% with a $70,000 payback.

I knew credit cards had outrageous interest rates of 18% and above, but I had no idea they were being outdone by orders of magnitude in the world of high finance.

Have a look at rates available in Utah from this company:

This is from LoanMe’s own website – with the next column in red calculated out by me and showing the total payoff.

For a $5,000 loan you’d be paying $36476.04 in interest over 7 years. For an even smaller loan of $2600, you would pay $15729.80 in interest over just shy of 4 years.

Predatory practices of this nature are incomprehensible; I thought we had laws against usury in this country, but I guess we don’t.

Be careful out there, and avoid those who would rob you in broad daylight under the loving protection of the law.

The Old Wolf has spoken.