I’m currently yanking the chain of an advance fee fraud scammer, much the same way I did over here. This one appears to be operating out of China. I’ll be posting a full report at the end of the game, but in the meantime, Mr. “Zhang Yong” has asked me to do some research for him so he can have a base of operations in the USA after all those “millions” have been transferred into my bank.

Just in case you’re wondering, these chests of money don’t exist.

See? This excellent certificate of deposit shows that I, personally, deposited lots of dollars into a Hong Kong bank.

Anyway, here’s the official request:

I am in receipt of your mail and the words in the contents made me happy that I finally got the right person for my proposal. As you have stated in your email that all monetary assets pertaining to this venture are confidently secure and that you are going to search for a business that will profit both of us. I will so much appreciate if you could start searching for a very nice four bed house with a very big garden located in a quiet environment conducive for learning.

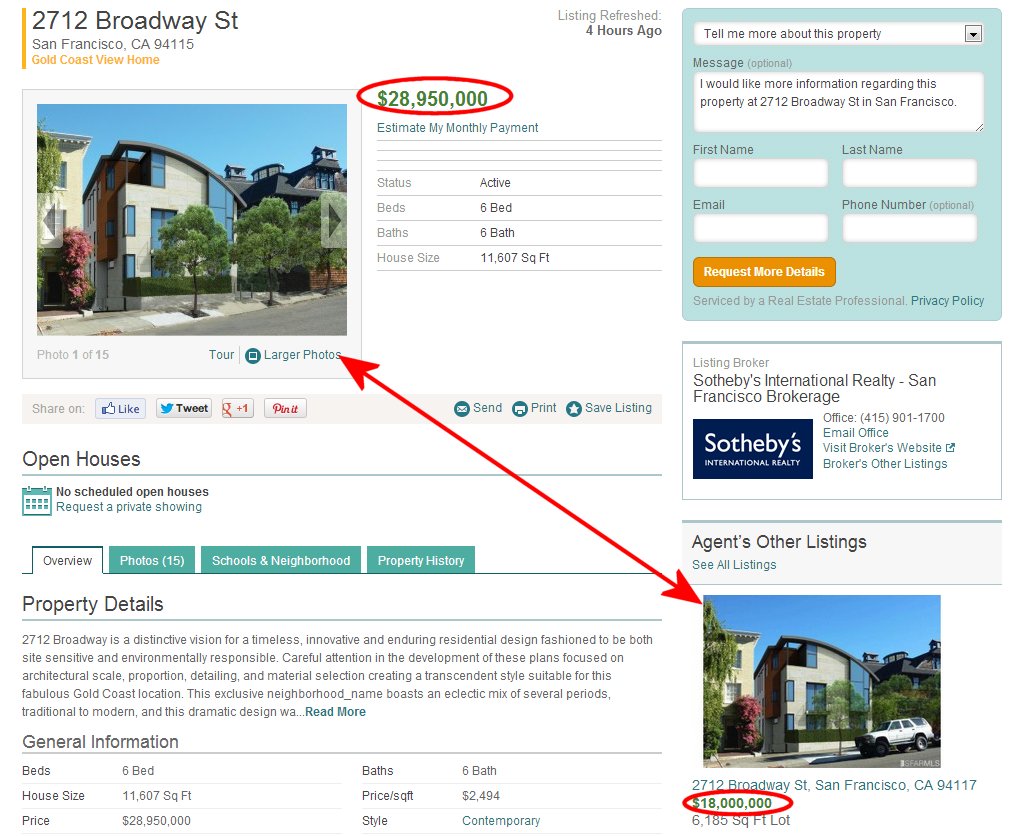

So I did a little research on the net and found this lovely property – a real one – for sale by Sotheby’s:

Only $28,950,000. Wow; a real steal. In addition, if you look closely at the page, you should be able to buy the same property in the Fringe Alternate Universe for about $11,000,000 less:

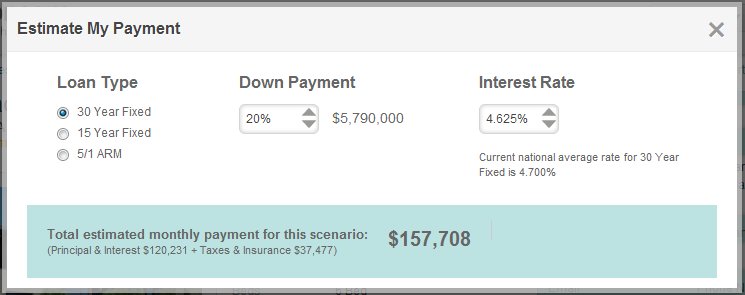

But seriously, assuming that the “Other Listing” is just an “oops” (I sent the agency a note letting them know that they might want to contact their webmaster, so the page probably won’t look like this for long), I allowed the monthly payment calculator to tell me how much this charming 4-bedroom property would be:

Assuming a $6 million down payment, your monthly charge would only be $157,708.

Cushlamochree. Who the hqiz has this kind of money? And this is only one of countless homes like this all over the place, in cities like New York and Boston and Los Angeles and San Francisco… and they’re selling.

Along with (cxhchhhxxttt paTOO!) Bank of America, we’re part owners of a 6-bedroom home in Central Utah. That monthly payment would just about buy our place every single month… for 30 years. I have a hard time getting my head around that kind of money… and it’s not lost on me that there are people in the world for whom $30,000,000 for a home would be considered petty cash. We just re-watched “Inception,” and I remember chuckling at this little exchange:

Cobb: For this to work, we’d have to buy off the pilots…

Arthur: And we’d have to buy off the flight attendants…

Saito: I bought the airline.

[Everybody turns and stares at him. Saito just shrugs]

Saito: It seemed neater.

Yes, it’s Hollywood – but let’s not kid ourselves – there are people like that out there.

It’s not a very nice world we live in when it comes to social equality; and, all things are relative. A large percentage of the world’s population would look at me and think I live like a potentate.

Our species deserves better, but how to overcome the massive inequality in wealth allocation without resorting to forced redistribution is a puzzlement.

“You cannot legislate the poor into freedom by legislating the wealthy out of freedom. What one person receives without working for, another person must work for without receiving. The government cannot give to anybody anything that the government does not first take from somebody else. When half of the people get the idea that they do not have to work because the other half is going to take care of them, and when the other half gets the idea that it does no good to work because somebody else is going to get what they work for, that my dear friend, is about the end of any nation. You cannot multiply wealth by dividing it.”

Dr. Adrian Rogers, 1931

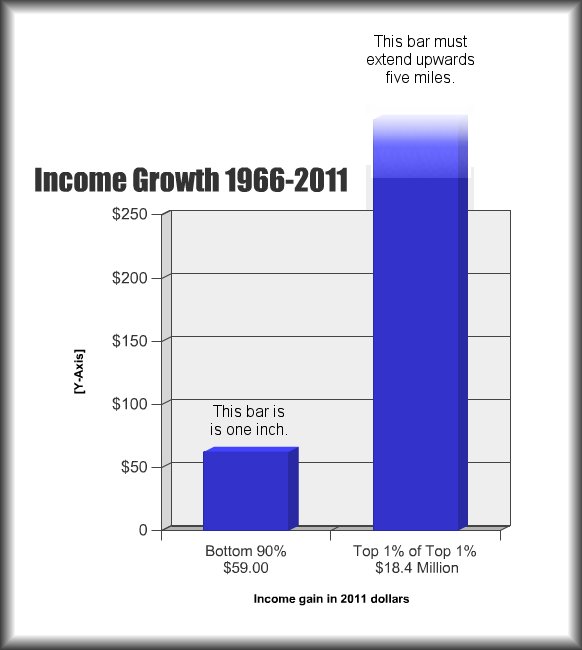

Those who would simply take from the rich and give to the poor ignore this at their peril, but the dangers of social leveling are only part of the problem. When I studied Economics in college – the only class I ever got a “C” in – one of the few concepts that really stuck was that at its base, money represents stored labor. This concept has been pretty much thrown in the trash; in our country, the Fed keeps creating new fiat dollars, and these are promptly snapped up by corporations and individuals who trade in the most complex, esoteric and incomprehensible instruments imaginable, not one of which has anything to do with work. It’s all smoke and mirrors, and as the recent bubbles (dotcom, housing, etc.) have shown, all of that wealth can vanish in a heartbeat.

More important than fixing the financial structure of our society would be fixing what goes on in the hearts of men; this article is a good spotlight on the depths of immorality to which humanity will sink when it comes to the gathering of money and power. One of my favorite quotes from entertainment comes from “Star Trek: First Contact”, when Picard explains to Lily,

“The economics of the future is somewhat different. You see, money doesn’t exist in the 24th century… The acquisition of wealth is no longer the driving force in our lives. We work to better ourselves and the rest of humanity.”

Please, make it so.

The Old Wolf has spoken.